In September, domestic steel prices fluctuated upwards. In September, affected by environmental protection measures such as “dual control”, domestic steel production continued to decline. The tightness of the steel market was expected to rise, and steel prices turned from a decline to an increase. Since October, steel prices have continued to rise slightly.

1. The domestic steel price index has turned from falling to rising

According to the monitoring of the Iron and Steel Association, at the end of September, China’s steel price index was 157.70 points, an increase of 6.63 points or 4.39% from the end of August, and a month-on-month increase; 51.71 points or 48.79% higher than the same period last year.

(1) The price increase of long products is higher than that of plates

At the end of September, the CSPI Long Products Index was 165.56 points, an increase of 12.49 points month-on-month, or 8.16%; the CSPI Plate Index was 154.19 points, a month-on-month increase of 1.59 points, or 1.04%; the price increase of long products was 7.12% higher than that of plates. Compared with the same period of the previous year, the long product and plate index increased by 56.82 points and 48.69 points, respectively, the increase was 52.25% and 46.15%.

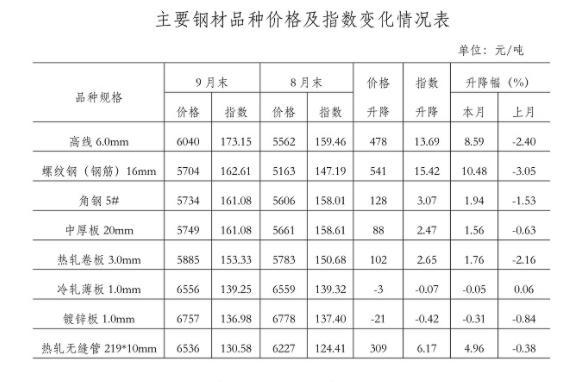

(2) Changes in the prices of major steel products

At the end of September, among the eight major steel products monitored by the Iron and Steel Association, the prices of cold-rolled sheet and galvanized steel fell slightly by 3 yuan/ton and 21 yuan/ton, respectively, and the prices of other varieties turned from falling to rising. Among them, high-speed wire, rebar, and hot-rolled seamless pipes rebounded greatly, with a month-on-month increase of 478 yuan/ton, 541 yuan/ton and 309 yuan/ton respectively; angle steel, medium and heavy plates and hot-rolled coils rose relatively small , The month-on-month increase was 128 yuan/ton, 88 yuan/ton and 102 yuan/ton respectively.

(3) Changes in the steel price index in each week

In September, the CSPI steel price index rose slightly every week; entering October, it continued to show an upward trend. National investment in fixed assets increased by 7.3% year-on-year, 1.6 percentage points lower than the growth rate from January to August. Among them, infrastructure investment increased by 1.5% year-on-year, down 1.4% from January to August; manufacturing investment increased by 14.8% year-on-year, down 0.9% from January to August; real estate development investment increased by 8.8% year-on-year, down from January to August A decline of 2.1 percentage points. In September, the value added of the industrial enterprises above designated size increased by 3.1% year-on-year, an increase of 0.05 percentage points from August; automobile production fell by 17.9% year-on-year, continuing to show a downward trend. Looking at the overall situation, the growth rate of the downstream steel industry fell in September, and the intensity of steel demand declined.

(4) Changes in steel prices in major regional markets

In September, the six major regional indexes of CSPI all changed from falling to rising. Among them, the market in East China has a relatively large increase, with a month-on-month increase of 4.93%; the Southwest region has a relatively small increase, with a month-on-month increase of 3.72%; North China, Northeast, Central South and Northwest China have increased by 3.74%, 4.23%, 4.35% and 4.58% respectively.

2. Analysis of the changing factors of steel prices in the domestic market

In September, affected by factors such as flood disasters and repeated epidemics in some areas, the demand side showed a slowdown; affected by the “dual control” measures, the supply side also declined. On the whole, both ends of the domestic steel market supply and demand are stable and slightly tight.

(1) The growth rate of the main steel industry slows down

According to data from the National Bureau of Statistics, in the first three quarters, GDP increased by 9.8% year-on-year, of which the third quarter increased by 4.9% year-on-year, a decrease of 3.0 percentage points from the previous quarter; the national fixed asset investment (excluding rural households) increased by 7.3% year-on-year, compared The growth rate in August dropped by 1.6 percentage points. Among them, infrastructure investment increased by 1.5% year-on-year, a decrease of 1.4 percentage points from January to August; investment in manufacturing increased by 14.8% year-on-year, a decrease of 0.9 percentage points from January to January; investment in real estate development increased by 8.8% year-on-year, down from January to August 2.1 percentage points. In September, the value added of the industrial enterprises above designated size increased by 3.1% year-on-year, an increase of 0.05 percentage points from August; automobile production fell by 17.9% year-on-year, continuing to show a downward trend. Looking at the overall situation, the growth rate of the downstream steel industry fell in September, and the intensity of steel demand declined.

(2) Crude steel production continued to decline month-on-month

According to the National Bureau of Statistics, in September, the national output of pig iron, crude steel and steel was 65.19 million tons, 73.75 million tons and 101.95 million tons, down 16.1%, 21.2% and 14.8% year-on-year, respectively. Crude steel output has been 5 consecutive The month-on-month decline, and the year-on-year decline for three consecutive months, and the rate of year-on-year decline accelerated month by month; the average daily crude steel production was 2.458 million tons, and the average daily month-on-month decline was 8.5%. According to customs statistics, in September, the country exported 4.92 million tons of steel, a decrease of 2.6% from the previous month; imported steel was 1.26 million tons, an increase of 18.2% from the previous month, and the net export of steel was 3.81 million tons of crude steel, a decrease of 530,000 tons from the previous month. Looking at the overall situation, the decline in steel production has offset the impact of weakening demand, and the supply and demand of the steel market have remained stable and slightly tight.

(3) The price of raw fuel materials fluctuates at a high level

In September, the price of iron ore dropped somewhat, but the prices of raw fuels such as coal coke and scrap steel continued to rise month-on-month. According to the monitoring of the Iron and Steel Association, at the end of September, the price of domestic iron concentrate dropped by 190 yuan/ton, and the price of CIOPI imported ore dropped by 33.72 dollars/ton; the prices of coking coal and metallurgical coke increased by 805 yuan/ton and 794 yuan/ton respectively. , The price of scrap steel increased by 38 yuan/ton from the previous month. Judging from the year-on-year situation, domestic iron concentrate and imported ore rose 8.80% and 2.82% year-on-year, the prices of coking coal and metallurgical coke rose 193.70% and 116.05% year-on-year, and the price of scrap steel rose 46.12% year-on-year. Iron ore, coal coke, and scrap steel prices remain high, pushing up the cost of steel for companies.

3. The international steel price has changed from rising to falling

In September, the international steel price index was 337.1 points, a month-on-month decrease of 0.7 points, or a decrease of 0.2%, from an increase to a decrease from the previous month; an increase of 182.3 points, or an increase of 117.8%, compared with the same period of the previous year.

International Steel Price Index (CRU) chart

(1) The long product index declined slightly, and the plate index continued to rise

In September, the CRU Long Products Index was 276.3 points, down 4.7 points month-on-month, or 1.7%; CRU Sheet Index was 367.4 points, up 1.4 points, or 0.4% month-on-month; compared with the same period last year, the CRU Long Products Index increased year-on-year 115.7 points, an increase of 72.0%; CRU plate index rose 215.6 points, an increase of 142.0%.

CRU Long Products and Plates Price Index Chart

(2) The rate of increase in North America has narrowed, the rate of decline in Europe has increased, and the rate of increase in Asia has shifted from rising to falling

1. North American market

In September, the CRU North American Steel Price Index was 440.2 points, an increase of 9.7 points from the previous month, or 2.3%, which was 2.9 percentage points lower than the previous month; the US manufacturing PMI was 61.1%, an increase of 1.2 percentage points from the previous month. Among them, the production index fell by 0.6 percentage points, and the inventory index rose by 1.4 percentage points; at the end of September, the U.S. crude steel capacity utilization rate was 84.59%, down 0.4 percentage points from the previous month. The prices of rebar and section steel from steel mills in the Midwestern United States remained stable this month, while other varieties continued to rise.

2. European market

In September, the CRU European Steel Price Index was 360.7 points, a month-on-month decrease of 4.4 points, or 1.2%, an increase of 1.8 percentage points from the previous month; the Eurozone manufacturing PMI was 58.6%, a month-on-month decrease of 2.8 percentage points. Among them, the manufacturing PMIs of Germany, Italy, France and Spain were 58.4%, 59.7%, 55% and 58.1%, respectively, which decreased from the previous month compared with the previous month. Except for the price of cold-rolled strip and coil, the prices of other types of flat products in the German market have declined this month.

3. Asian market

In September, the CRU Asian Steel Price Index was 263.5 points, a month-on-month decrease of 4.7 points, or 1.8%, from an increase to a decrease from the previous month; Japan’s manufacturing PMI was 51.5%, a decrease of 1.2 percentage points from the previous month; South Korea’s manufacturing PMI was 52.4%, The month-on-month increase was 1.2 percentage points; China’s manufacturing PMI was 49.6%, a decrease of 0.5 percentage points from the previous month. In the Indian market this month, except for the continuous recovery of steel and wire prices, the prices of other varieties continued to decline, and the rate of decline narrowed from the previous month.

Fourth, analysis of later steel price trends

As the weather turns colder, the demand for downstream steel has decreased. In order to ensure the reduction of crude steel output throughout the year, various localities and departments have further increased relevant policies and measures, and steel output will also be reduced in the later period. In the later period, market supply and demand are basically stable, and steel prices will fluctuate slightly. The domestic market has entered the off-season of steel consumption, and the demand intensity has weakened. From the perspective of the international market, the global economic recovery is showing an unstable trend. According to the latest World Economic Outlook issued by the International Monetary Fund in October, it is predicted that the global economy will continue to recover in 2021, but due to the impact of the epidemic, the momentum of recovery has weakened. It is estimated that the global economy will grow by 5.9% throughout the year, which is 0.1% lower than the forecast value in the July report. The impact on the global supply chain and the pressure of inflation have increased the risks to the global economic outlook. From the perspective of the domestic situation, the operation of the national economy is also under downward pressure. The GDP growth rate in the third quarter was 4.9%, which was significantly lower than the growth rate in the second quarter. Under the policy constraints of housing and non-speculation, there are signs of further weakness in later real estate investment, the scale of local debt issuance, and the financing of real estate enterprises; the level of orders in the machinery industry has continued to decline, and the growth of automobiles has continued to decline. In the later period, the demand for steel showed a further weakening trend.

(1) Production reduction policy continues, market supply and demand are expected to stabilize

Premier Li Keqiang proposed at the meeting of the State Council’s Energy Commission on October 9 that “persist in a game of chess across the country, do not rush, proceed from reality, and correct some localities with “one size fits all” power curtailment or “exercise-style” carbon reduction”. For the steel industry, this does not mean that the task of reducing crude steel production has changed. Judging from the current situation, the state resolutely suppresses crude steel output and strictly adheres to the bottom line of not adding new capacity. The relevant ministries and commissions are organizing a nationwide “look back” inspection of steel capacity reduction and the reduction of crude steel output, mainly producing steel. Large provinces and large steel companies have also introduced measures to control crude steel output. It is expected that crude steel output will still decline in the later period. Overall, both ends of supply and demand are expected to form a new level of stability, and steel prices will fluctuate slightly.

(2) The social stock of steel has turned from decline to increase, and corporate stocks continue to rise

According to the statistics of the Iron and Steel Association, in early October, the social inventory of five types of steel in 20 cities across the country was 10.85 million tons, an increase of 200,000 tons or 1.9% from the end of September. Million tons, an increase of 48.6%; a decrease of 1.79 million tons or 14.2% over the same period of the previous year. From the perspective of corporate inventory, in early October, the steel inventory of member steel companies was 12.84 million tons, an increase of 890,000 tons or 7.43% from the end of September; an increase of 1.22 million tons or 10.51% from the beginning of the year; and a decrease of 75% from the same period last year. 10,000 tons, down 5.52%. Both social stocks of steel and corporate stocks have risen, and it is difficult for steel prices to rise sharply in the later stage.

The main issues that need to be paid attention to in the later period:

First, the output of crude steel has fallen sharply, and a new balance between supply and demand is expected to form in the later period. Domestic crude steel production has continued to decline year-on-year, and the rate of decline has increased, and the intensity of steel demand for downstream demand has also weakened. Iron and steel enterprises should carefully analyze the market demand situation, actively adjust product structure, and maintain stable steel prices.

Second, the prices of coking coal and coke are consolidating at a high level, and enterprises are still under pressure to reduce costs and increase efficiency. According to the monitoring of the Iron and Steel Association, on October 15, the prices of coking coal and metallurgical coke were 3,815 yuan/ton and 4,118 yuan/ton, respectively, up 156.38% and 76.36% from the beginning of the year, while the steel price index rose only 27.76% in the same period. The price of coal and coke continues to be high, putting greater pressure on steel companies in the later stages to reduce costs and increase efficiency.

Your message must be between 20-3,000 characters!

Your message must be between 20-3,000 characters!