According to CCTV survey, cultural paper dropped by more than 2,000 yuan per ton

As an important upstream production material, the price of pulp has fluctuated in the past six months. In late August, the price of pulp dropped by 1.2% compared to mid-August. What impact does this have on paper companies?

After visiting several paper mills, the reporter found that the current ex-factory price of cultural paper used for writing and printing is about 5100-5300 yuan per ton. This price has fallen by more than 2,000 yuan from the highest point of more than 7,000 yuan per ton in May. At the same time, the prices of wood pulp raw materials such as hardwood pulp and softwood pulp have also declined in the past two months.

Li Zonghui, assistant to the general manager of China Metallurgical Paper Galaxy Co., Ltd.: When the price of softwood pulp was more than 7,000 yuan/ton, it was adjusted back by about 1,000 yuan, and it is currently stable at more than 6,000 yuan/ton. The price of hardwood pulp is at a high level of 6000 yuan/ton, to the price of 4600/ton and 4700 yuan/ton.

Data show that in 2020, the total imported wood pulp across the country will reach 30.64 million tons, accounting for 72.8% of total wood pulp consumption. Industry insiders analyze that, at present, the overall domestic demand for paper remains stable, and the price of pulp is expected to stabilize.

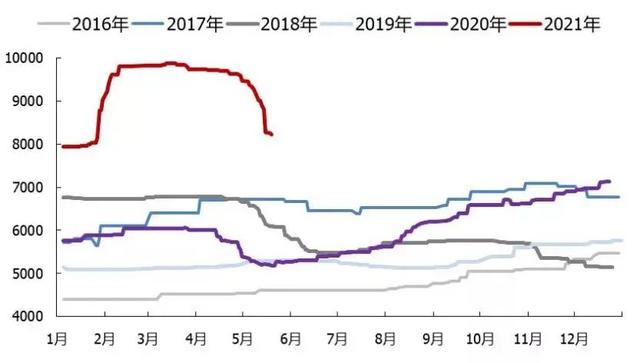

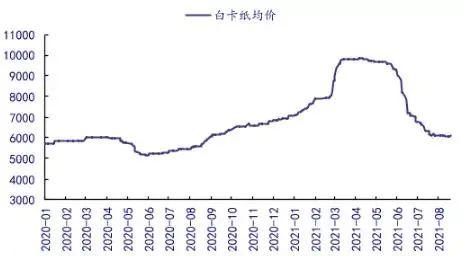

The price of white cardboard cut in half

From January 1, 2021, the “Waste Ban” has been fully implemented, which has further promoted the “replacement of plastic with paper”, and the demand for biodegradable paper cups, paper bowls, lunch boxes and other paper products has increased.

The dividend of the national policy pushed up the price trend of white cardboard. The “Opinions on Further Strengthening the Treatment of Plastic Pollution” clearly stipulates that by the end of 2020, many places in China will comprehensively restrict the use of non-degradable plastic bags. After the implementation of the policy, white cardboard, the main product of “replacing plastic with paper”, became a hot commodity. The industry conservatively estimates that about 1 to 3 million tons of new paper packaging demand will be released every year, of which over 90% is the demand for white cardboard.

Among the current applications of white cards, social cards (packaging boxes for medicines, cosmetics, 3C digital, etc.) account for 60%, cigarette cards 26%, and food cards 14%. As the sales of medicines, foods, 3C products, and cosmetics increase year by year, white cardboard, which is the main force of commodity packaging, has better quality and toughness. Under the trend of consumption upgrading, it has gradually replaced low-end white cardboard and is widely used in mass consumer products. White cardboard has become one of the popular alternative materials in fields such as lunch boxes used in catering takeaways and paper bags in contact with food.

In this context, on January 25, 2021, the leading domestic paper industry companies announced price increases, announcing that they will increase by 500 yuan/ton from February to March, and a new wave of price increases is coming. At this time, the price of white cardboard rose to 7,500 yuan/ton. In March, the white cardboard market once again made efforts to announce price increases, and the price soared all the way to 1,000 yuan/ton. At this point, the price of white cardboard has broken through historical records and officially entered the 10,000 yuan era. From then on, the price of white cardboard remained high in April and May.

In the first half of 2021, the trend of white cardboard has shown an inverted U-shaped trend. Since the second quarter, the paper industry has entered a traditional off-season. The early growth rate of white cardboard has been too fast, and the purchase cost of downstream customers has soared, forming a more obvious wait-and-see and resistance to the market. Psychology. Downstream medium- and large-scale printing plants have begun to actively cut orders or choose to purchase raw materials with lower costs. The cold operation in the early stage has prompted the current downstream manufacturers to have ample stocks and overdraft market demand in advance.

At the same time, with the repeated global public health incidents, the import of overseas epidemics, and the superposition of multiple factors such as the policy of ensuring the supply and stabilization of bulk commodities, the industry has seen contradictions between supply and demand, and the price of white cardboard basically showed a downward trend in the second half of the year.

·In the short term, supported by tight supply and demand and wood pulp prices, the price of white cardboard is expected to remain high;

·The long-term release of large-scale production capacity may bring prices back to low levels.

The release of policy dividends at the beginning of the year drove a substantial increase in the performance of many leading listed companies in the paper industry in the first half of the year. In mid-April, the price of white cardboard began to decline slowly, and began to enter a rapid decline pattern at the end of May, until the market decline slowed down at the end of July. The market price of mainstream brand white cardboard in the market in August was about 6,110 yuan/ton, which was a drop of 38% from the 10,000 yuan/ton price at its peak, which was almost “halved.”

In the future, with the arrival of the traditional peak season of Golden Nine and Silver Ten, the domestic epidemic has been effectively controlled, and the marginal influencing factors have obviously weakened. The domestic demand for white cardboard may rebound, and the demand side can be slightly alleviated.

However, the new crown epidemic continues to show repeated outbreaks around the world, the problem of shipping containers has not yet been alleviated, and rigid shipping issues such as prices and cycles continue to hinder exports, and orders that rely on foreign trade exports are more severely affected. Potential market risks still exist. As the prices of pulp and other commodities fall, it is expected that white cardboard will not rise in the short term, and it is likely that the trend of white cardboard will not be prosperous in the peak season of Gold, September, and Silver.

Your message must be between 20-3,000 characters!

Your message must be between 20-3,000 characters!